Electronic Components Sales Market Analysis and Forecast (July 2025)

Table Of Contents

Prologue

1 Macroeconomics in July

1.1 The Manufacturing Industry Is Operating Weakly

1.2 Investment in the Electronic Information Manufacturing Industry Has Declined

1.3 Semiconductor Sales Remain Strong

2 Chip Delivery Trend in July

2.1 The Overall Chip Delivery Trend

2.2 List of Delivery Cycles of Key Chip Suppliers

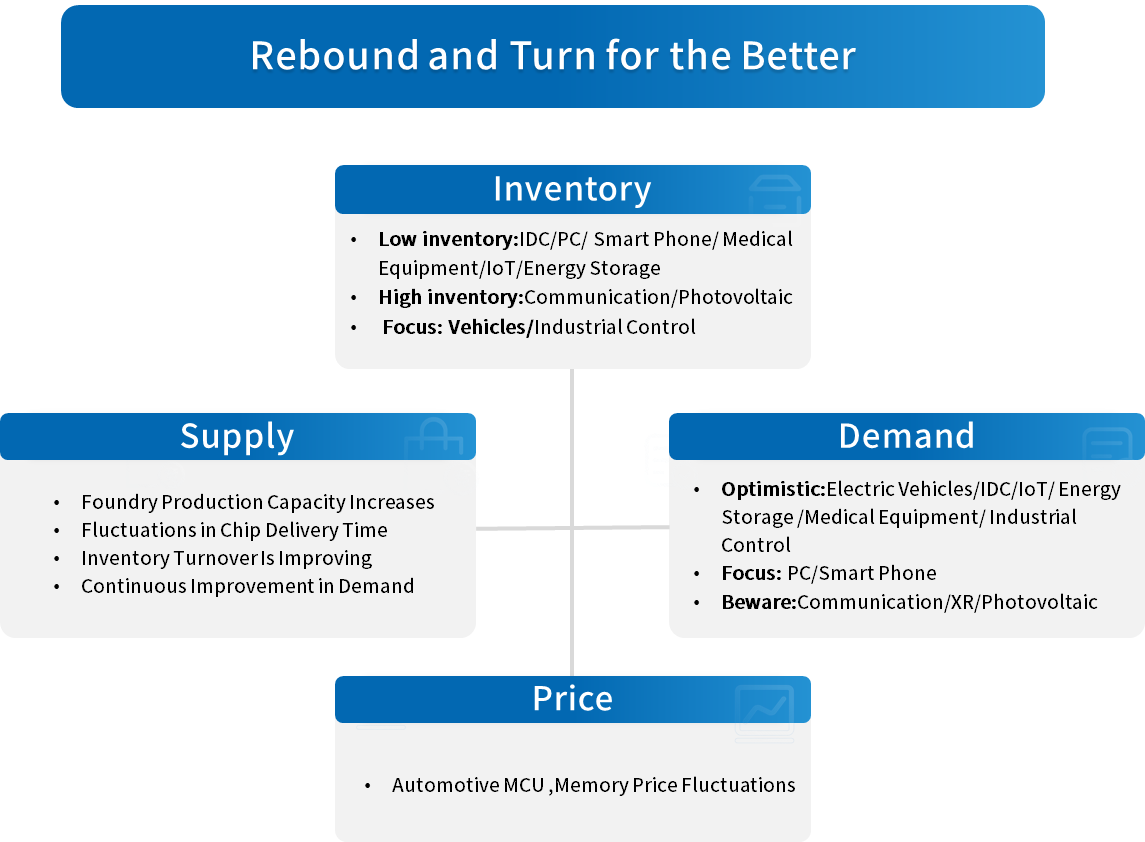

3 Orders and Inventory in July

4 Semiconductor Supply Chain in July

4.1 Semiconductor Upstream Manufacturers

(1)Silicon Wafer/Equipment

(2)Fabless/IDM

(3)Foundry

(4)OSAT

4.2 Distributor

4.3 System Integration

4.4 Terminal Application

(1)Consumer Electronics

(2)New Energy Vehicles

(3)Industrial Control

(4)Photovoltaic

(5)Energy Storage

(6)Data Center

(7)Communication

(8)Medical Equipment

5 Distribution and Sourcing Opportunities and Risks

5.1 Opportunities

5.2 Risk

6 Summarize

Disclaimer

Prologue

1 Macroeconomics in July

1.1 The Manufacturing Industry Is Operating Weakly

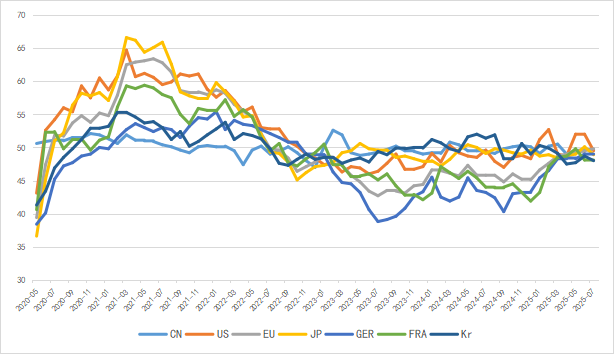

In July, the global manufacturing PMI dropped slightly, and the economy continued to operate weakly. Among them, China, the United States, Japan, and South Korea saw significant declines, while EU countries such as Germany and France rebounded. With the continued uncertainty in U.S. tariff policies, the situation of insufficient effective market demand has not changed significantly, and the global economic recovery still faces substantial downward pressure.

The World Bank's latest forecast shows that the global trade growth rate is expected to slow from 3.4% last year to 1.8%. It is worth noting that the IMF has raised its forecast for China's economic growth this year from 4% in April to 4.8%, and major international organizations are optimistic about the prospects of China's economic recovery.

Chart 1: Manufacturing PMI of the world's major economies in July

Source: NBSPRC

1.2 Investment in the Electronic Information Manufacturing Industry Has Declined

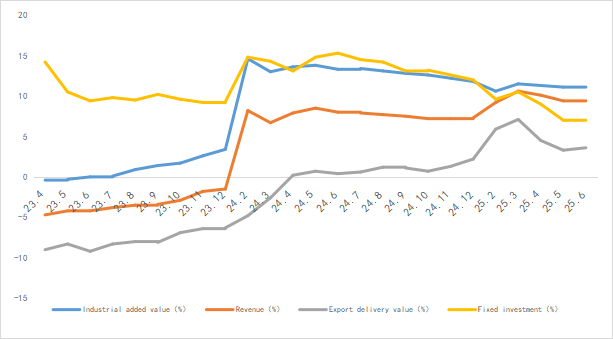

In the first half of 2025, China's electronic information manufacturing industry achieved rapid production growth, with exports maintaining a stable and positive momentum, continuous improvement in efficiency, a slight decline in investment, and the overall development of the industry remained sound.

Chart 2: Latest Operation of Electronic Information Manufacturing Industry

Source: MIIT

1.3 Semiconductor Sales Remain Strong

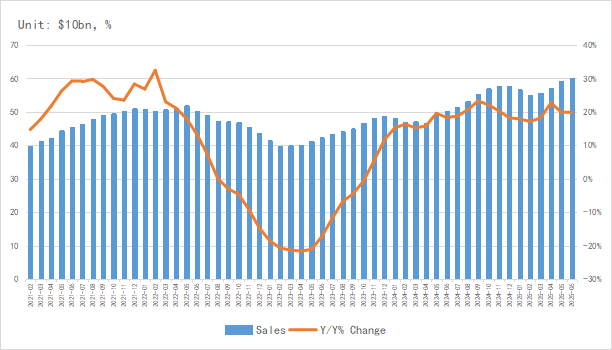

According to the latest data from SIA, the global semiconductor market sales reached $59.91 billion in June 2025, a year-on-year increase of 19.6%, marking the 14th consecutive month with a year-on-year growth rate exceeding 17%. SIA predicts that the annual growth will occur in the second half of the year.

In terms of regional markets, the growth in the Americas market has slowed down, with a year-on-year increase of 24.1%.the Chinese mainland saw a year-on-year growth of 13.1%, the Asia-Pacific region grew by 34.2% year-on-year, while sales in Japan and Europe were -2.9% and 5.3% respectively. Asia-Pacific markets such as China have become new growth drivers.

Chart 3: Latest global semiconductor industry sales and growth rate

Source: SIA,Chip Insights

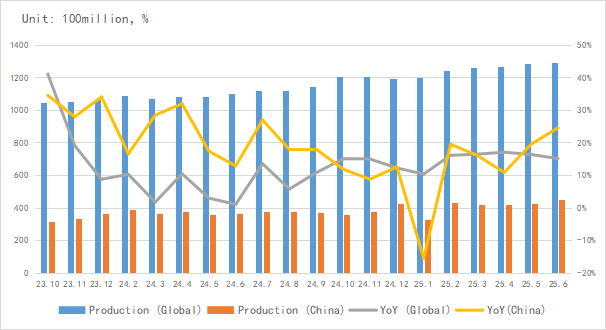

In terms of integrated circuit output, the global integrated circuit output in June was approximately 129.1 billion units, a year-on-year increase of over 15%.China's output exceeded 45.06 billion units, with a cumulative output of 239.47 billion units from January to June, showing a trend of rapid growth.

Chart 4: Latest global and Chinese integrated circuit production and growth rate

Source: NBSPRC,SIA,Chip Insights

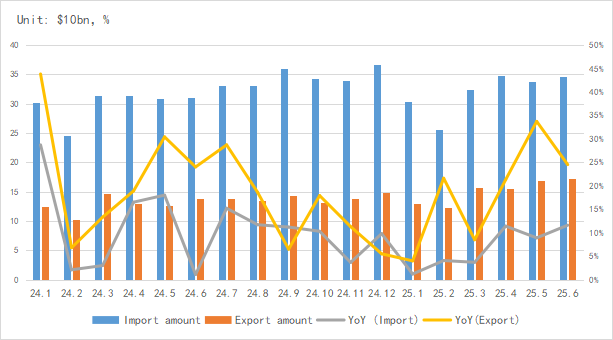

In terms of import and export, China's integrated circuit exports maintained high growth in June, with a growth rate exceeding 21% for three consecutive months.

Chart 5: Latest import and export amount and growth rate of integrated circuits in China

Source: MIIT,SIA,Chip Insights

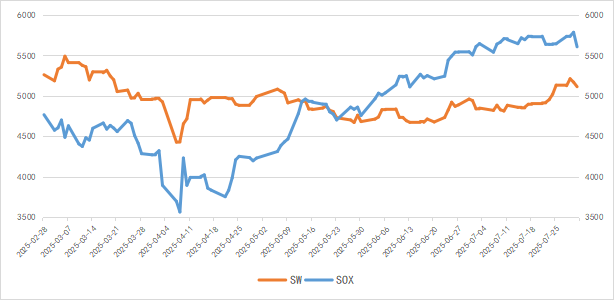

From the perspective of capital market indices, the SOX index rose by 1.8% in July, and China's Semiconductor (SW) Industry Index increased by 3.5%, indicating a recovery in the prosperity of the semiconductor capital market.

Chart 6: Trend of SOX and SW Index in July

Source: Wind,Chip Insights

For more information, please refer to the attached report.