Electronic Components Sales Market Analysis and Forecast (April 2026)

Table Of Contents

Prologue

1 Macroeconomic Situation in April

1.1 Global Manufacturing Sentiment Improves, Economy Recovers Steadily

1.2 Electronic Information Manufacturing Sees Improved Profitability and Strong Exports

1.3 Semiconductor Sales Remain Strong, Driven by Asia-Pacific Market

2 Chip Lead Time Trends in April

2.1 Overall Chip Lead Time Trends

2.2 Overview of Lead Times for Key Chip Suppliers

3 Order and Inventory Status in April

4 Semiconductor Supply Chain in April

4.1 Upstream Semiconductor Manufacturers

(1)Silicon Wafer/Equipment

(2)Fabless/IDM

(3)Foundry

(4)OSAT

4.2 Distributor

4.3 System Integration

4.4 Terminal Application

(1)Consumer Electronics

(2)New Energy Vehicles

(3)Industrial Control

(4)Photovoltaic

(5)Energy Storage

(6)Data Center

(7)Communication

(8)Medical Equipment

5 Distribution and Sourcing Opportunities and Risks

5.1 Opportunities

5.2 Risk

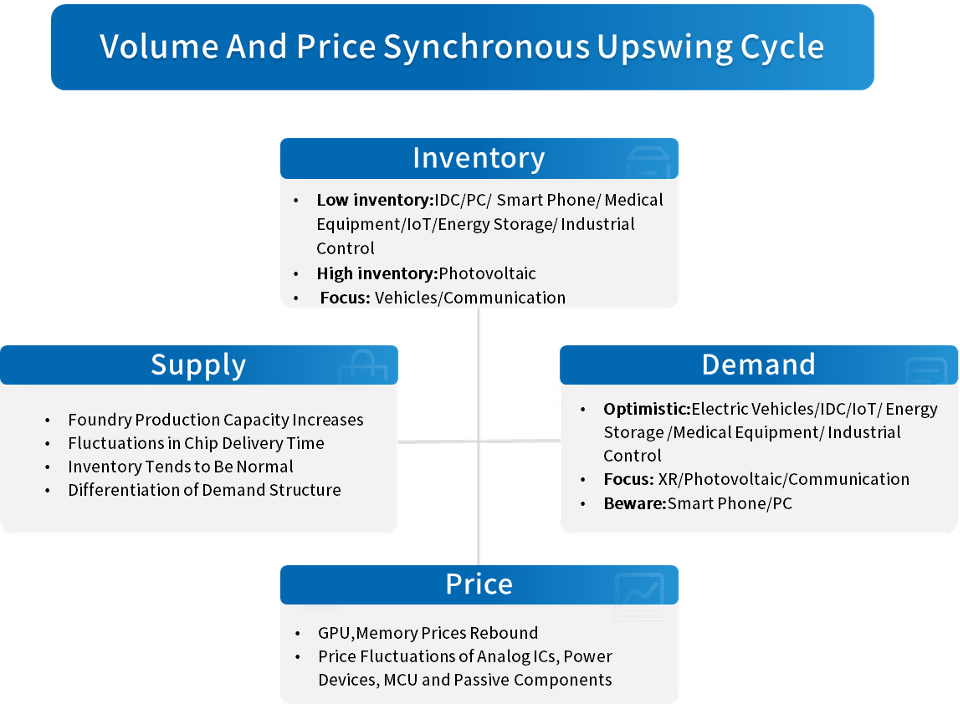

6 Summarize

Disclaimer

Prologue

1 Macroeconomic Situation in April

1.1 Global Manufacturing Prosperity Continues with Moderate Growth

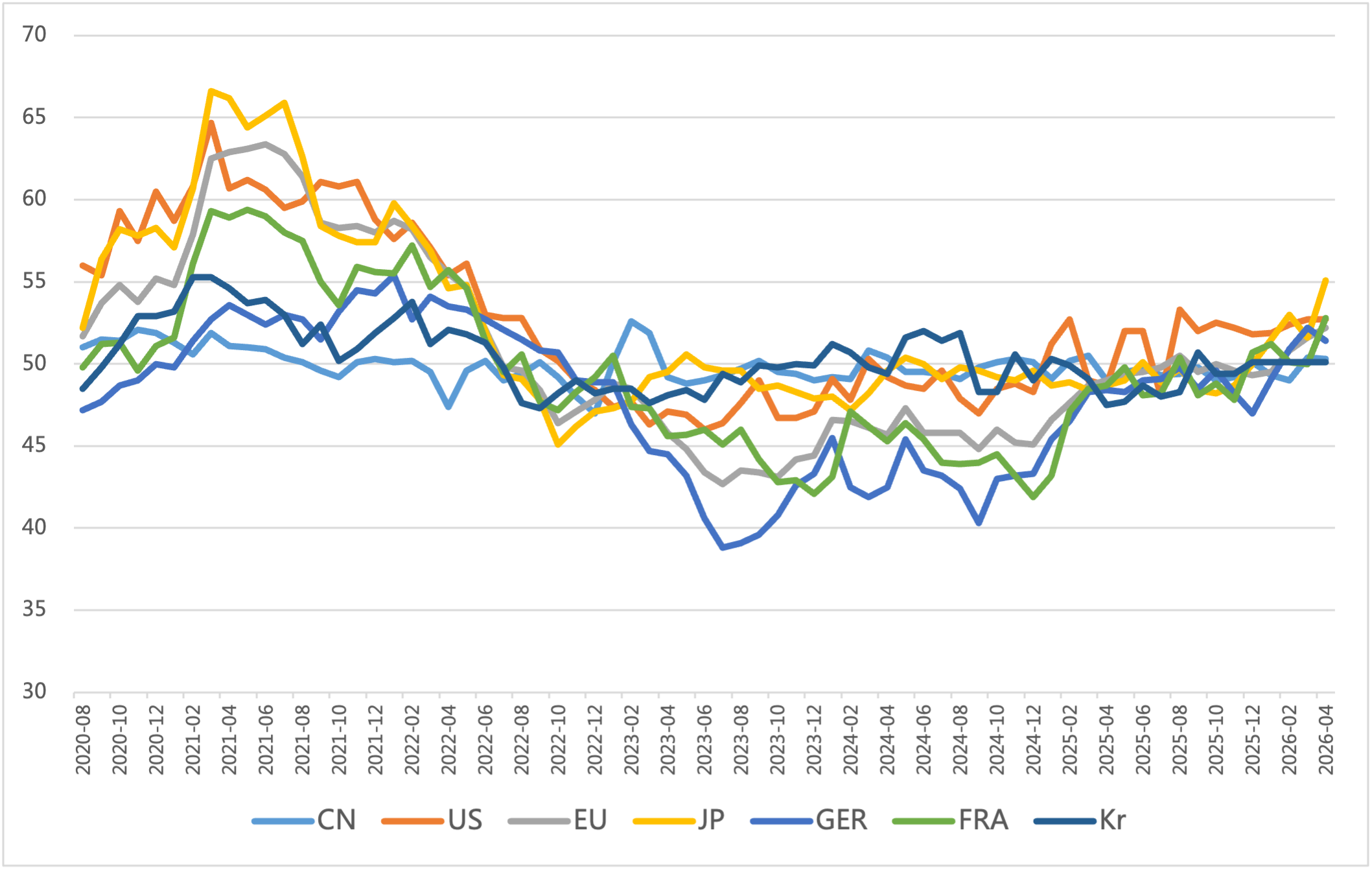

In April, the global manufacturing PMI posted steady growth and extended the expansion cycle. Major economies including China, the EU, the United States, Japan and South Korea all remained above the boom-bust threshold. The economy is expected to recover steadily and improve further. It is worth noting that external impacts such as Middle East geopolitical tensions persist. Commodity markets fluctuate frequently and uncertainties remain prevalent.

Chart 1: Manufacturing PMI of the world's major economies in April

Source: NBSPRC

1.2 Electronic Information Manufacturing Sees Improved Profitability and Sound Momentum

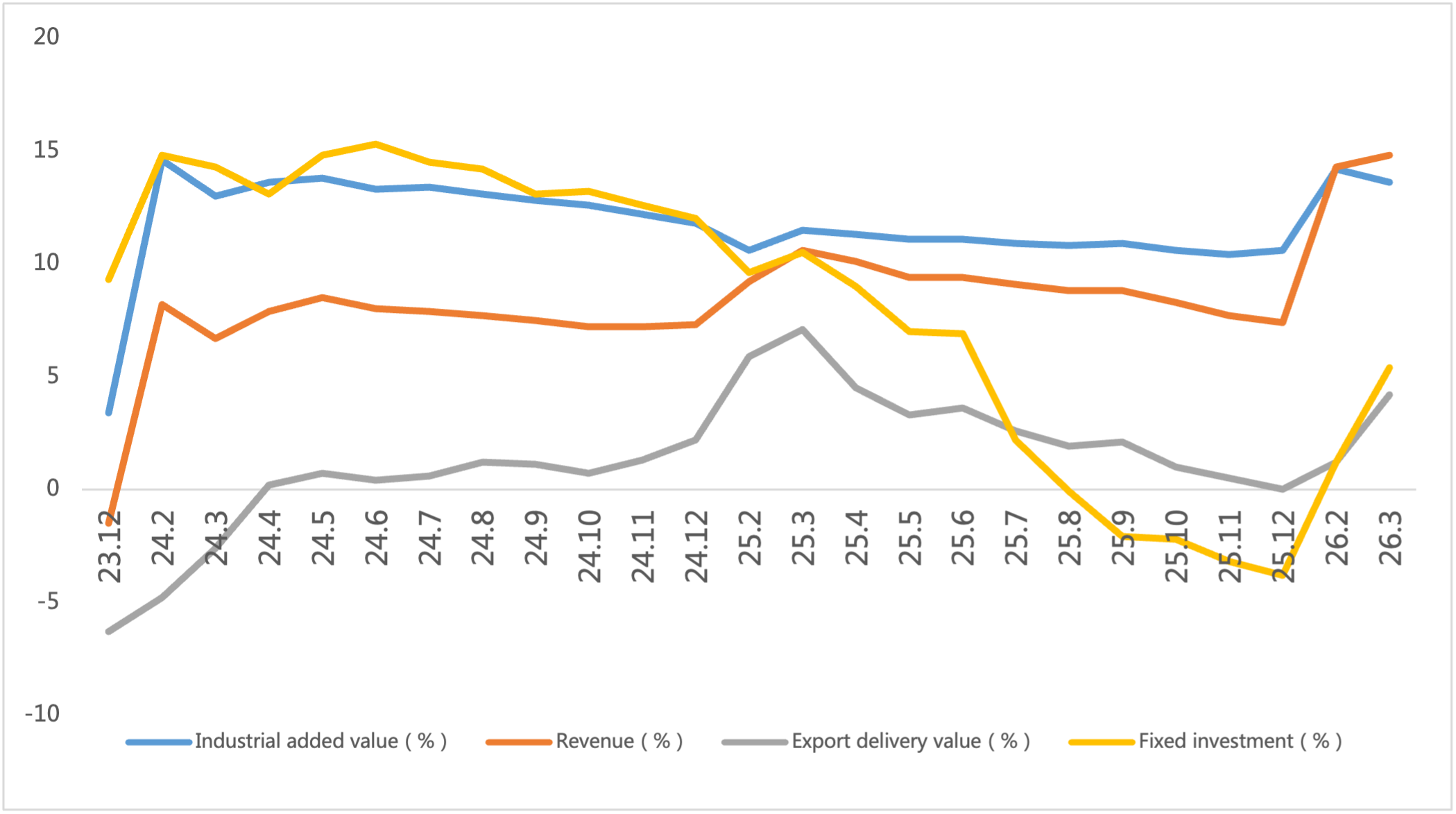

In Q1 2026, China’s electronic information manufacturing industry achieved rapid production growth. Exports kept rebounding, profitability improved substantially, and investment growth accelerated, presenting a solid overall industrial performance.

Chart 2: Latest Operation of Electronic Information Manufacturing Industry

Source: MIIT

1.3 Semiconductor Sales Remain Strong Led by China and the US

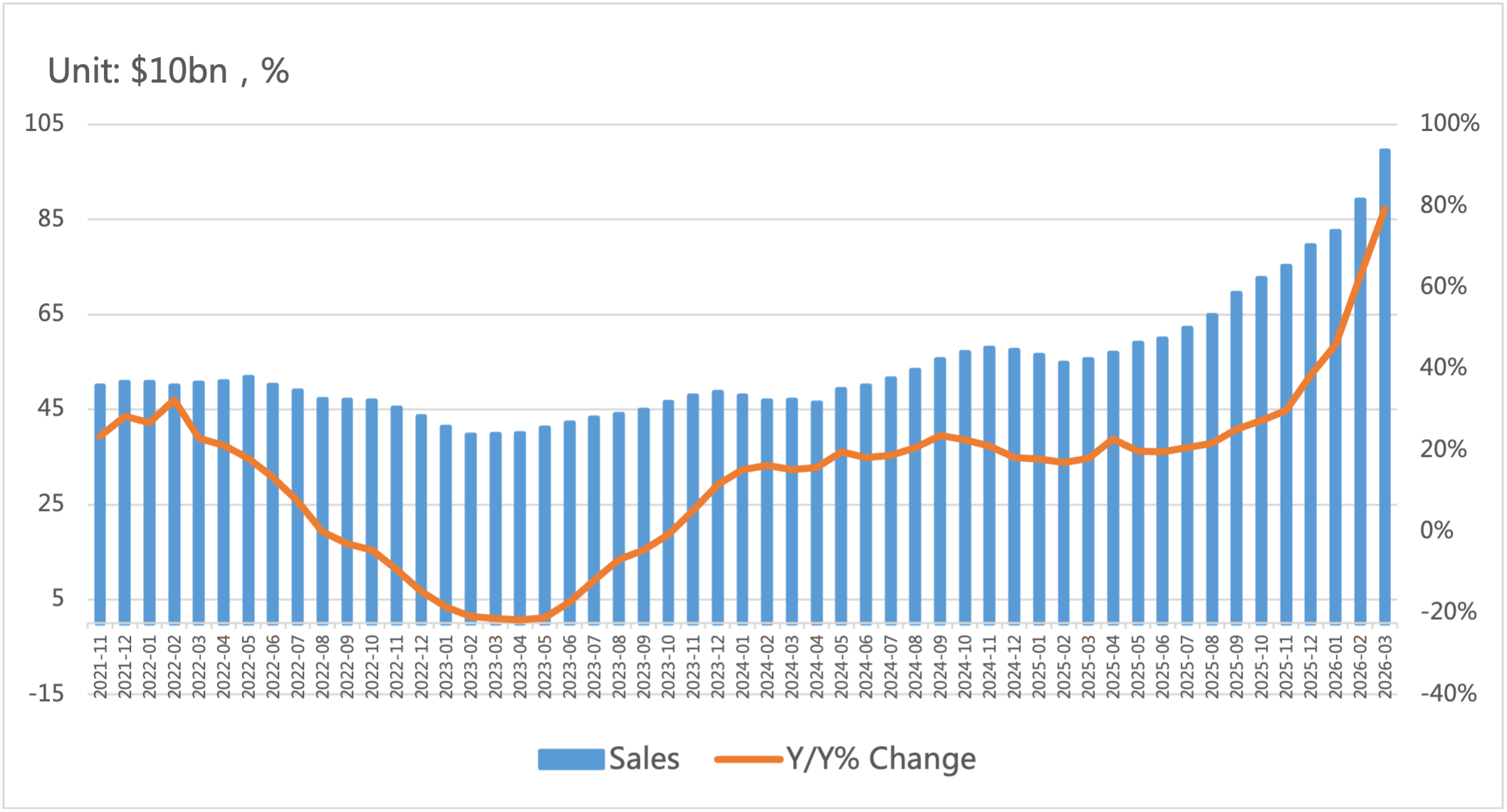

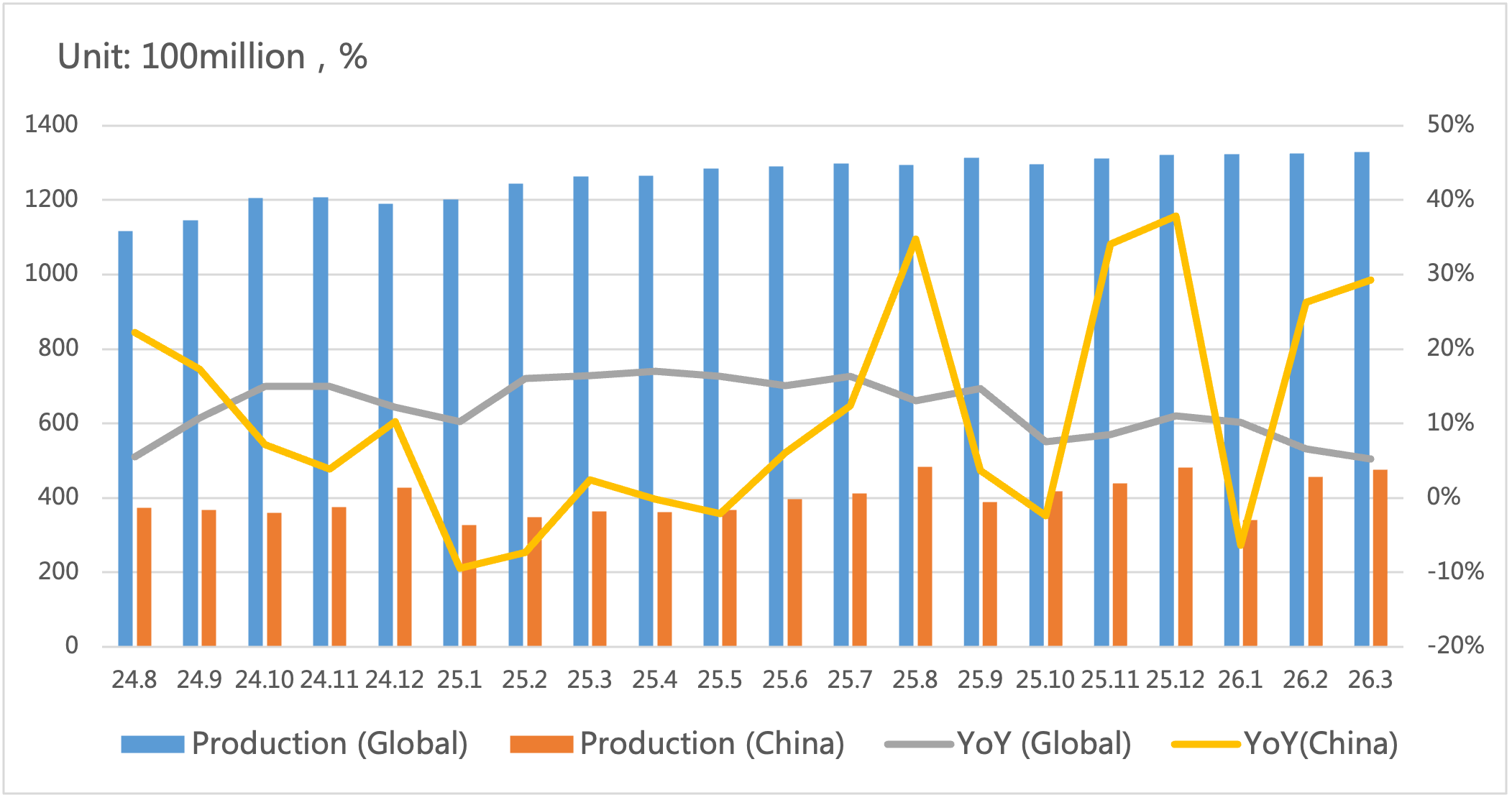

In terms of integrated circuit output, global and China’s IC production exceeded 132.9 billion units and 47.5 billion units respectively in March, maintaining an upward momentum.

Chart 3: Latest global semiconductor industry sales and growth rate

Source: SIA,Chip Insights

In terms of integrated circuit output, China's cumulative IC production exceeded 81.5 billion units in February, maintaining an upward trend in line with global capacity.

Chart 4: Latest global and Chinese integrated circuit production and growth rate

Source: WSTS,SIA,Chip Insights

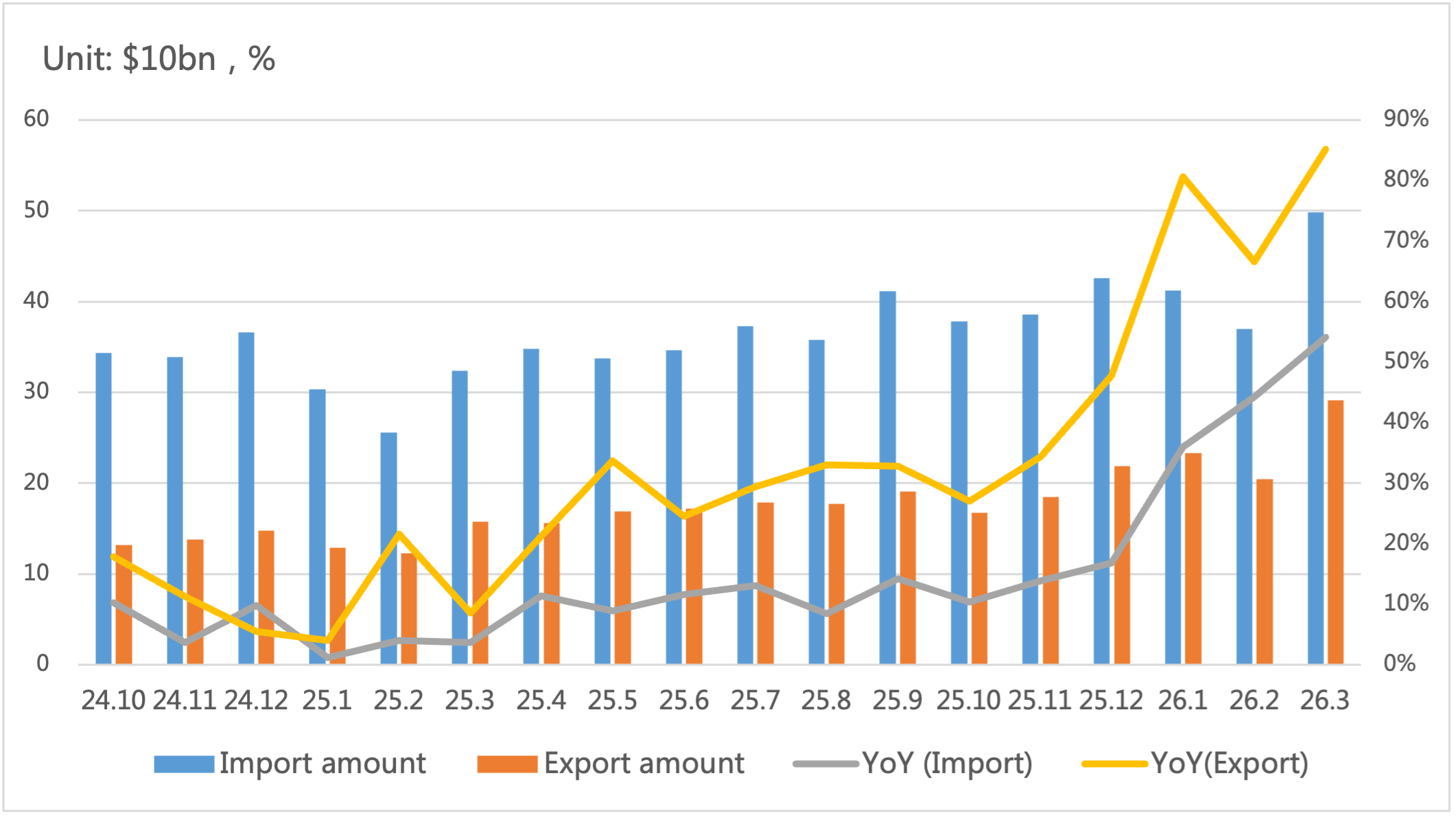

In terms of imports and exports, China’s IC trade maintained robust growth in March. Imports and exports rose by more than 54% and 85% year-on-year respectively.

Chart 5: Latest import and export amount and growth rate of integrated circuits in China

Source: MIIT,SIA,Chip Insights

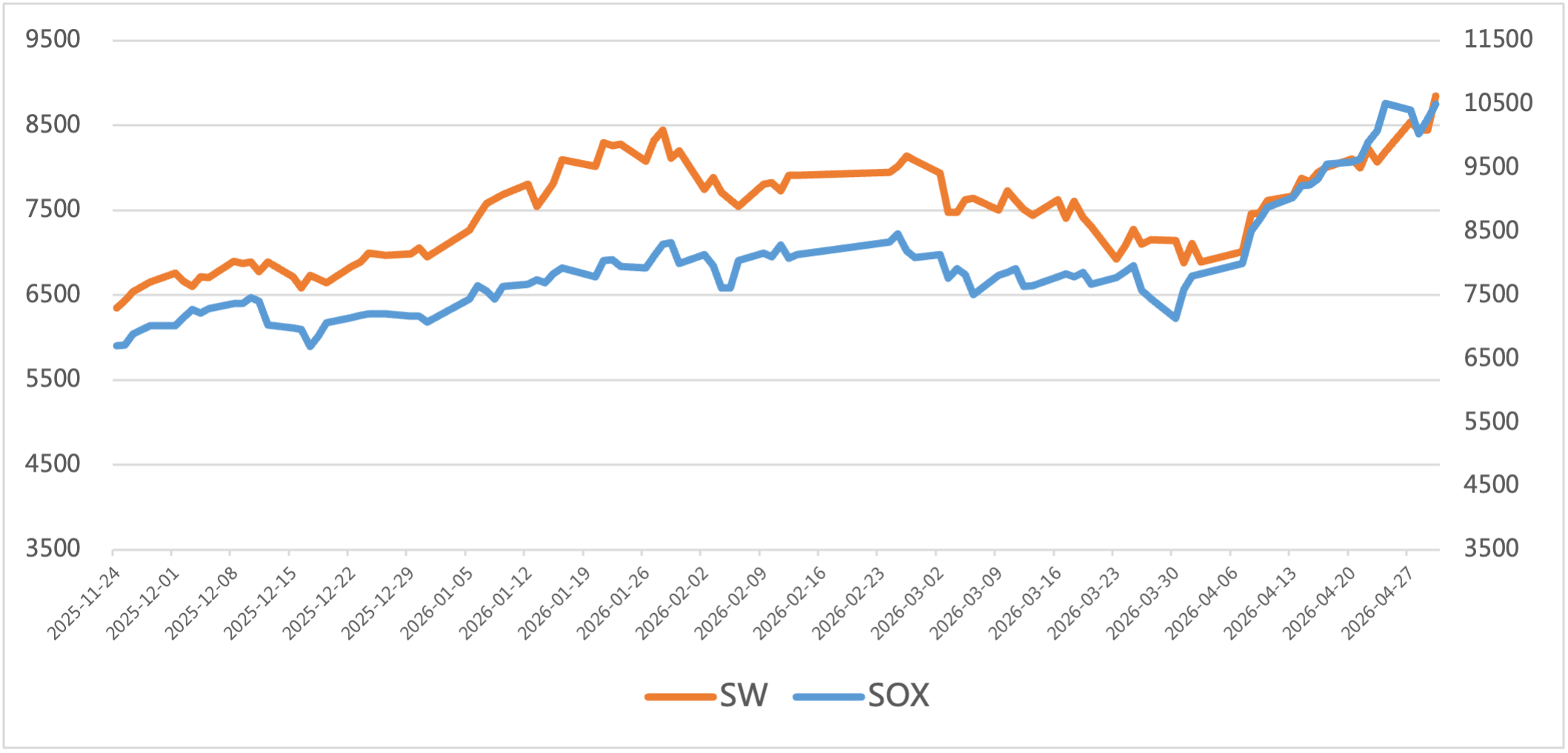

From the capital market perspective, the Philadelphia Semiconductor Index (SOX) rose by 34.2% in April, while the China Semiconductor (SW) Industry Index increased by 24.4%. Market linkage with overseas sectors and improved performance of leading enterprises jointly drove the indices higher.

Chart 6: Trend of SOX and SW Index in April

Source: Wind,Chip Insights

For more information, please refer to the attached report.