Electronic Components Sales Market Analysis and Forecast (February 2026)

Table Of Contents

Prologue

1 Macroeconomic Situation in February

1.1 Global Manufacturing Maintains Expansion with Lingering Uncertainties

1.2 Electronic Information Manufacturing Achieves Steady Growth with Sound Momentum

1.3 Robust Semiconductor Sales Fuel Optimistic Market Outlook Led by China

2 Chip Lead Time Trends in February

2.1 Overall Chip Lead Time Trends

2.2 Lead Time Overview of Key Chip Suppliers

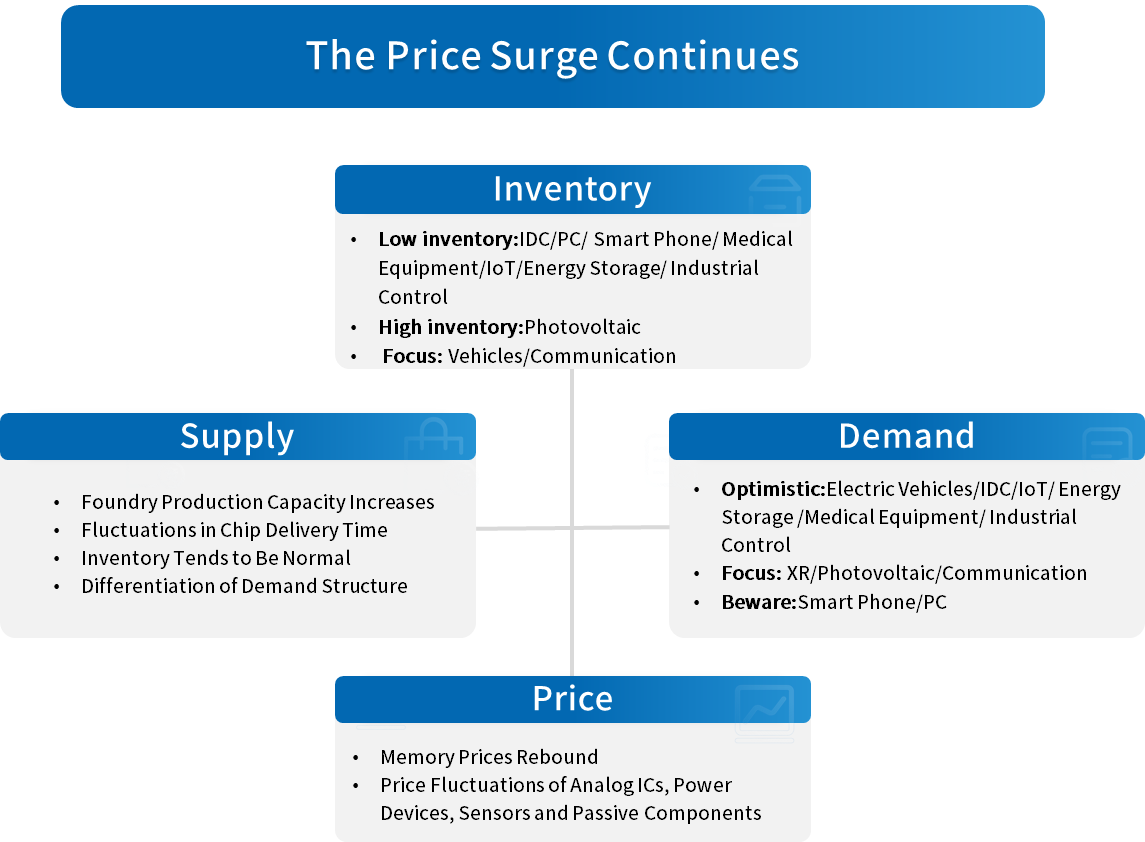

3 Order and Inventory Status in February

4 Semiconductor Supply Chain in February

4.1 Upstream Semiconductor Manufacturers

(1)Silicon Wafer/Equipment

(2)Fabless/IDM

(3)Foundry

(4)OSAT

4.2 Distributor

4.3 System Integration

4.4 Terminal Application

(1)Consumer Electronics

(2)New Energy Vehicles

(3)Industrial Control

(4)Photovoltaic

(5)Energy Storage

(6)Data Center

(7)Communication

(8)Medical Equipment

5 Distribution and Sourcing Opportunities and Risks

5.1 Opportunities

5.2 Risk

6 Summarize

Disclaimer

Prologue

1 Macroeconomic Situation in February

1.1 Global Manufacturing Maintains Expansion with Lingering Uncertainties

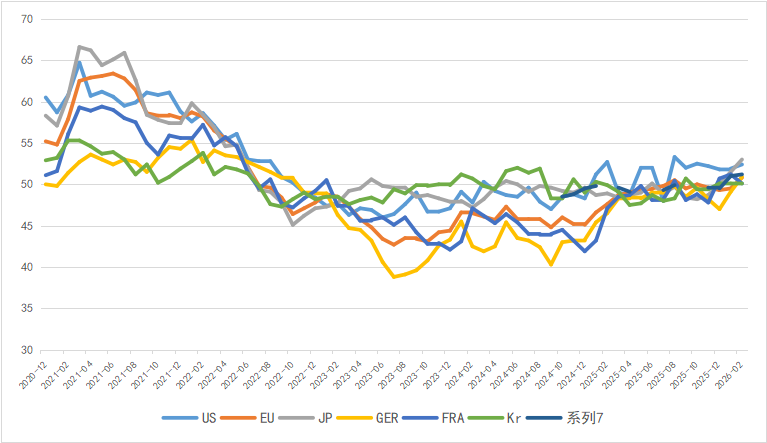

In February, the global manufacturing PMI continued its moderate expansion, with a notable rebound in Europe. Except for China, the EU, the US, Japan and South Korea all stayed above the boom-bust line. Among them, the euro zone manufacturing PMI surged to 50.8 in February, a 44-month high, driven primarily by the strong performance of Germany's manufacturing sector.

Looking ahead to the full year, the recovery shows positive signs, yet the escalating geopolitical risks in the Middle East may exacerbate the uncertainty of the recovery.

Chart 1: Manufacturing PMI of the world's major economies in February

Source: NBSPRC

1.2 Electronic Information Manufacturing Achieves Steady Growth with Sound Momentum

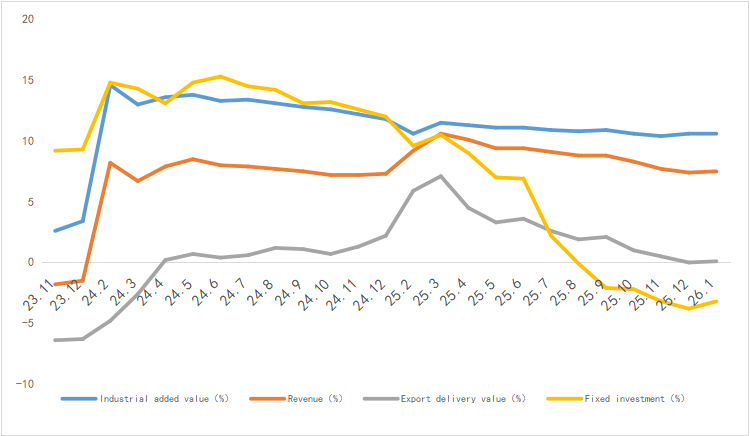

In January 2025, China's electronic information manufacturing industry witnessed stable production growth, steady improvement in efficiency, stable exports and investment, and the industry maintained a sound development momentum overall.

Chart 2: Latest Operation of Electronic Information Manufacturing Industry

Source: MIIT

1.3 Robust Semiconductor Sales Fuel Optimistic Market Outlook Led by China

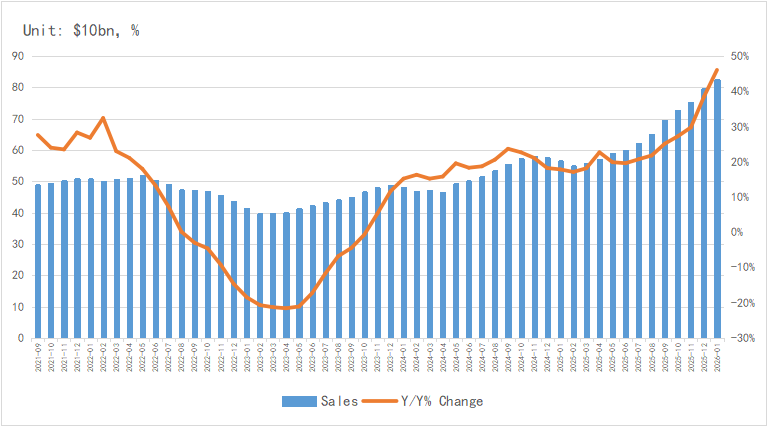

According to the latest data from the SIA, the global semiconductor market sales reached 80.24 billion US dollars in January, a year-on-year increase of 46.1%, maintaining a growth rate of over 20% for seven consecutive months.

In terms of regional markets, the American market grew by 34.9% year-on-year, while the Asia-Pacific region represented by China saw a year-on-year increase of 47.0%. Japan and Europe recorded sales growth rates of -6.2% and 26.1% respectively. SIA expects the Asia-Pacific market including China to be the main growth driver this year.

Chart 3: Latest global semiconductor industry sales and growth rate

Source: SIA,Chip Insights

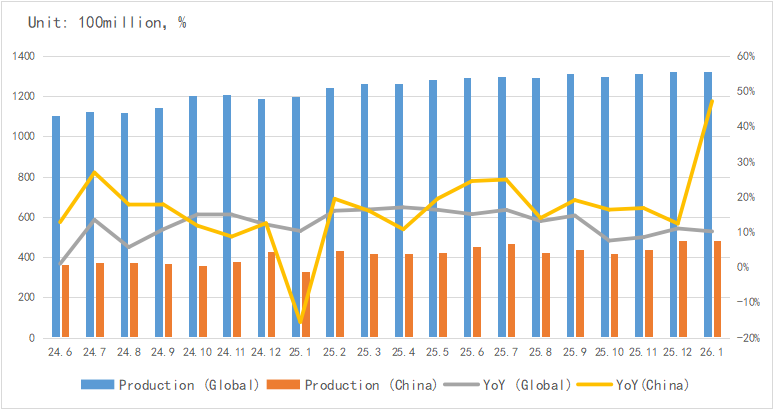

In terms of integrated circuit output, the global and Chinese integrated circuit output both exceeded 130 billion units and 48 billion units respectively in January, with production capacity continuing to rise.

Chart 4: Latest global and Chinese integrated circuit production and growth rate

Source: WSTS,SIA,Chip Insights

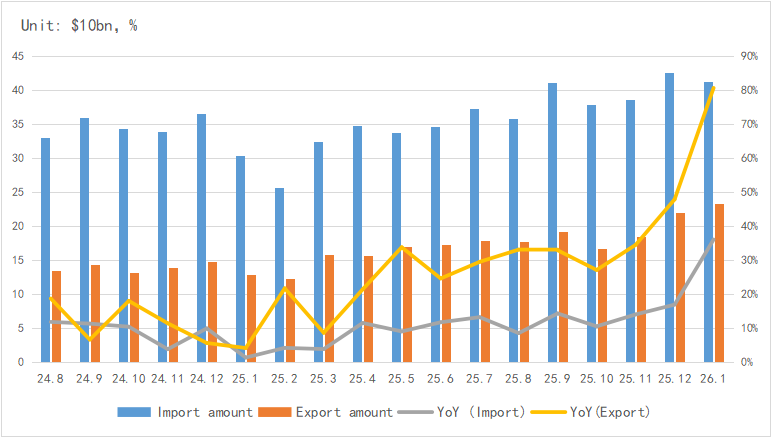

In terms of imports and exports, China's integrated circuit exports maintained a high growth in January, with an average growth rate of over 25% for 13 consecutive months.

Chart 5: Latest import and export amount and growth rate of integrated circuits in China

Source: MIIT,SIA,Chip Insights

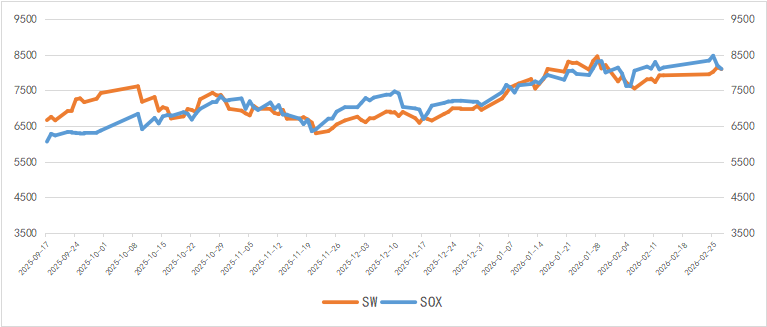

From the perspective of capital market indices, the Philadelphia Semiconductor Index (SOX) fell by 0.4% in February, while China's Semiconductor (SW) Industry Index edged up by 4.4%, indicating a relatively stable capital market with high prosperity.

Chart 6: Trend of SOX and SW Index in February

Source: Wind,Chip Insights

For more information, please refer to the attached report.